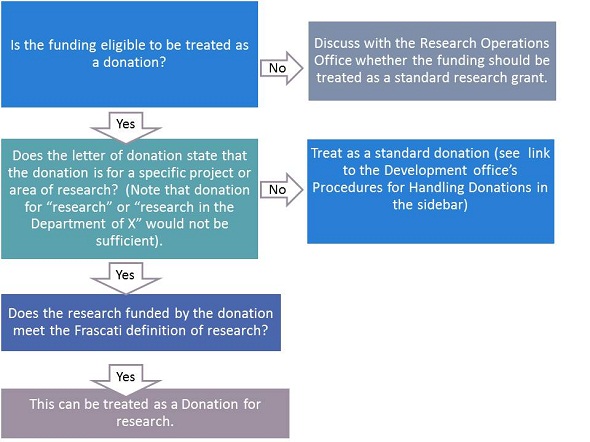

For a donation to be set up as a research grant, the following criteria must be met:

- The terms of a gift must reflect the fact that it is a donation (e.g. no IP rights to the donor)

- The donor’s intention to make the donation for a specific research project or area must be clear at the outset and documented between the donor and the University

- The research activity must meet the Frascati definition of research

- The gift must be spend-down or, in rare instances if held as a trust fund, this must be a non-permanent endowment whereby spend is allowed against the principal

- Only expenditure against principal can be counted towards research income (spend against interest, where this applies, cannot be counted because interest is categorised as internally-generated income)

Process for determining whether or not funding is eligible to be treated as a 'Donation for Research':